By David Bowcott

Driving Better Project Outcomes Through Better Risk Data

Construction industry project budgets have far too much capital allocated to unknown costs and risks. Sure, construction is an industry fraught with many unknowns, but with advancements in data science and technologies that allow us to better capture and organize data, it seems like it might be a good time to rethink the way capital is allocated when setting a budget.

Traditional construction budgets combine direct costs, unknown costs (contingencies), and profits to arrive at a final construction price. Direct costs are easily defined. These are costs to develop the project design, procure project materials, and construct project materials in line with the project design.

More challenging is the fact that the construction industry has perhaps the most unknown risks (costs) of any industry. To manage these unknown risks, a substantial amount of capital is allocated on most projects as a “shock absorber.” The two primary unknown risks on a construction project are profit and contingency. A third source of project capital, and one that is often overlooked when it comes to unforeseen project costs/risks, are the premiums given to insurers and surety companies to take on traditional insurable risks.

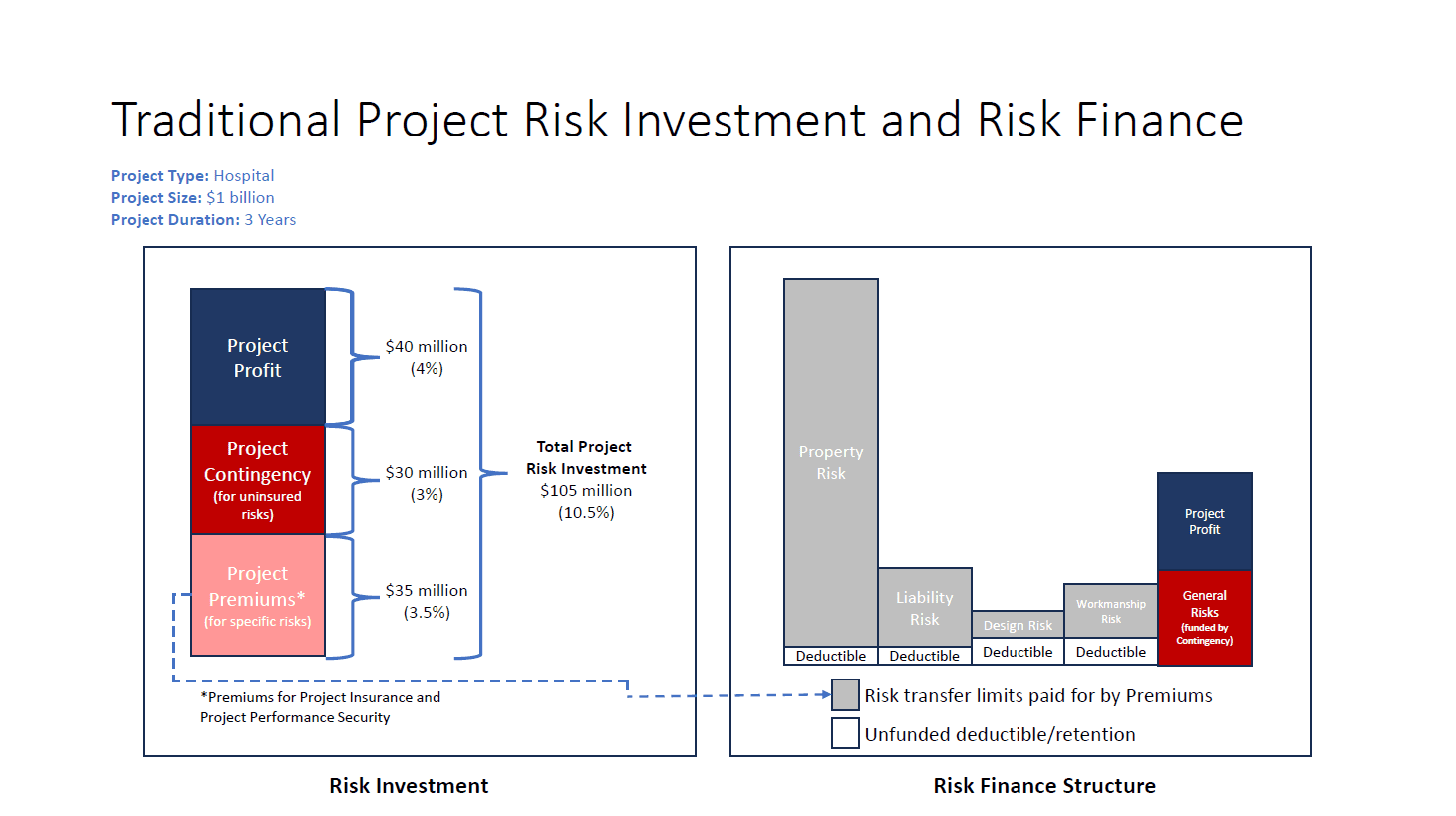

Figure 1 – Traditional project risk management investment and risk finance structures

Using Data Science

Given advancements in data science, and technologies that more effectively capture construction data, there appears to be clear opportunity for the construction industry to re-allocate these three sources of shock absorber capital to more precisely manage known and unknown risks, and to drive better project outcomes.

Figure 1 is an example of how these three sources of project shock-absorber capital are traditionally invested and how they are generally used to finance project risks. This example imagines a $1 billion hospital project with a three-year construction duration. As you can see, the combined amount of project capital that is used to arrive at project profit, project contingencies and project premium is substantial — in excess of 10 per cent of the construction budget. Under these traditional structures, there is no mingling of the insurance/surety premiums used to finance traditionally insurable project risks, and the contingency and profit funds which are used to fund uninsurable costs/risks.

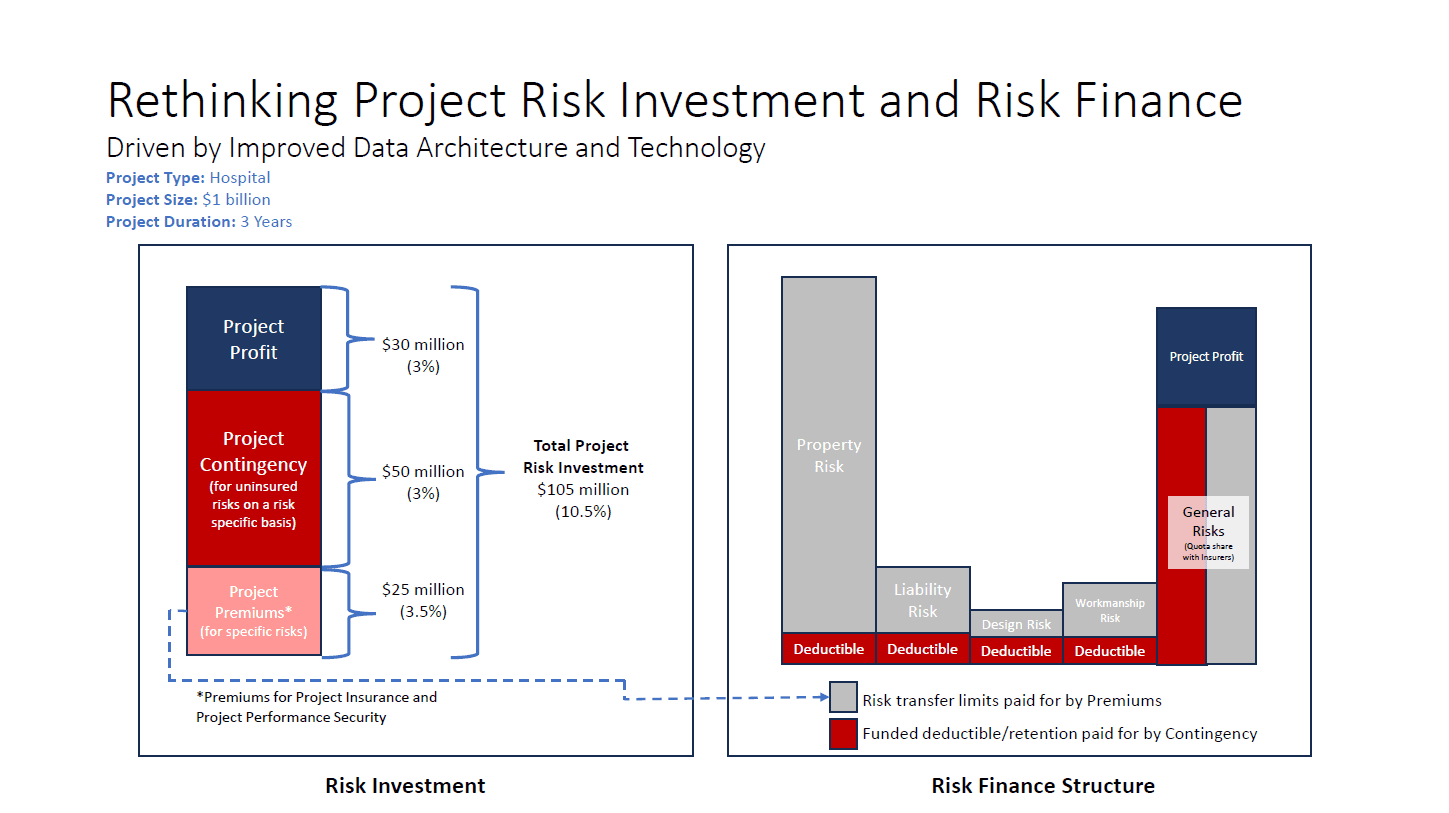

Fig 2 – Rethinking project risk management investment and risk finance (a more risk specific allocation of project “shock absorber” capital

Fig 2 – Rethinking project risk management investment and risk finance (a more risk specific allocation of project “shock absorber” capital

Rethinking the Structures

With access to tools that can better quantify probability and severity of all project risks, both insurable and uninsurable, could the construction industry devise a risk finance structure that co-mingles these three sources of project capital? And if there is such a structure, what would that look like?

Figure 2 illustrates a potential structure that represents a rethinking of the way project shock-absorber capital could be reallocated and better integrated with the more risk-specific framework of insurance and performance security covers. In this structure, you see more of the project profit being temporarily allocated to project contingency with the project contingency being broken into a more risk-specific framework. The project contingency is now funding the previously unfunded deductibles/ retentions, and a higher retention level is being put forward for each of the project insurance covers. This reduces premium spend, given a greater level of risk retention, and there is a more creative way to fund uninsured risks by creating a quota share structure with insurance/ performance security capital. This novel risk investment and risk finance structure creates several potential benefits.

It presents a more efficient and better thought-out process for identifying and financing project risk. It is a more granular approach than just having a pool of capital for all risks not insured. Such a framework, once fully developed, will make the “go or no-go” decision making framework more effective. There is also less money being transferred, and forever lost, to the insurance sector. There is also a potential to create more funding for uninsured losses using quota-share structure for general risks.

Given that deductibles/retentions are funded (either fully or partially) using project continency and profit, and given these funds are allocated on a risk specific, more granular basis, it becomes possible to use these funds to drive better adherence to risk controls through the potential bonusing of a portion of these funded retentions. Such frameworks have been proven effective, with subcontractor default insurance and retrospective programs for workers compensation in the United States being good examples.

A much more thoughtful approach to managing project risk should result in better risk management story to share with insurance partners, and potentially your clients, as well as other construction stakeholders. A rethinking of how project capital is allocated can drive better project outcomes, but a key first step to creating such a structure is to develop a solid data architecture or data strategy, and to begin harnessing the power of construction technologies to better capture, organize and analyze project data.

These discussions may be a compelling reason to bring together key management within your company, including the CFO, COO, CTO/CIO and risk manager, to rethink the way project profit, project contingency and project premiums are combined and structured.

This article is a repost from On-Site Magazine, originally published on October 4, 2024.

Questions? Contact:

David Bowcott, Executive Vice President

David Bowcott, Executive Vice President

Construction Industry Group

dbowcott@platforminsurance.com

416-566-5973