Update on Construction Insurance Market – How Construction Market Trends are Impacting the Construction Insurance Sector

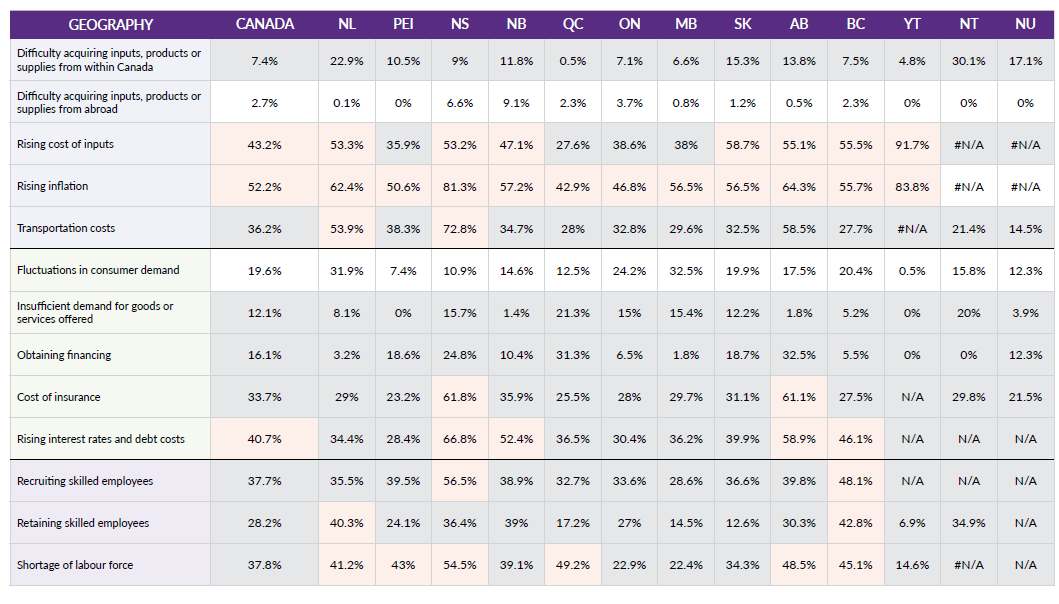

Every quarter the Canadian Construction Association (CCA) publishes their ICIC Construction Insights document. Included in this document is a “Survey of Business Obstacles” that outlines the various pain points the Canadian construction sector is dealing with (i.e., inflation, access to skilled labour, demand for construction, etc.). One of the highest charting pain points over the last few quarterly surveys has been the Cost of Insurance. Below is a copy of the latest survey results:

Source: Canadian Construction Association (CCA) ICIC Construction Sector Quarterly Insights (published Aug 2024)

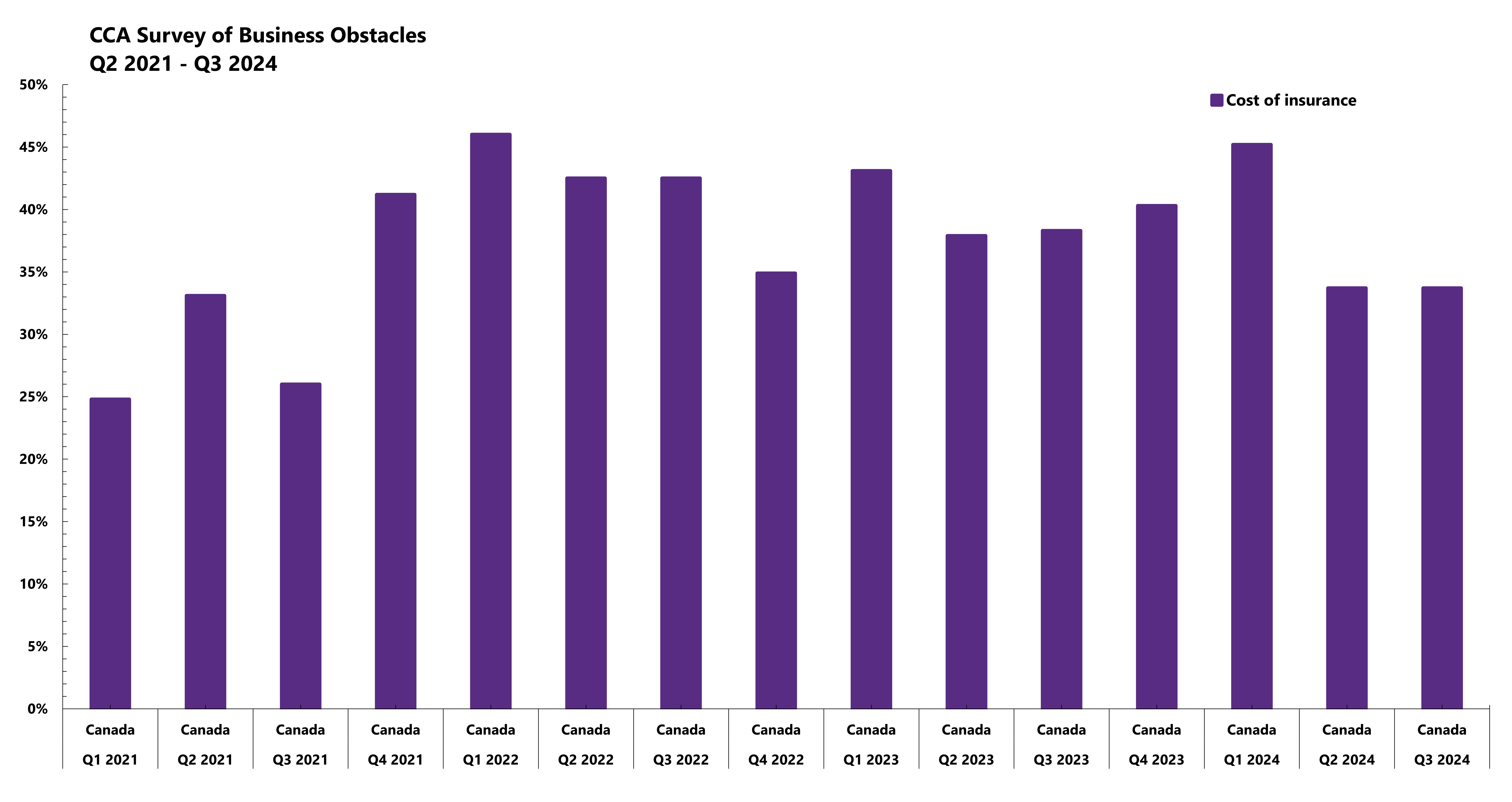

As you can see, across Canada 33.7% of all respondents to the survey indicated the cost of insurance is an obstacle to doing business, with the Provinces of Nova Scotia and Alberta showing over 60% of their respondents citing cost of insurance as an obstacle. The following chart shows the percentage of construction stakeholders that see the cost of insurance as an obstacle in their businesses over the past 15 quarters:

Source: Canadian Construction Association (CCA) Survey of Business Obstacles

As you can see over 1 in 3 construction stakeholders have considered the cost of insurance an obstacle for the past 12 quarters in a row – evidence that the hard market which began in 2018 continues to take its toll on the Canadian construction industry.

WHAT CONSTRUCTION TRENDS ARE DRIVING INCREASED INSURANCE COSTS?

- Larger Projects – Project sizes have become larger and larger over the past several decades. With larger projects comes larger insurable losses making insurers less profitable and driving increased pricing.

- Uniqueness of Projects – In recent study done by Bent Flyvbjerg he concluded the more unique a project is, the greater likelihood that that project will have cost overruns. Today’s construction economy has many unique projects being constructed which is driving greater cost overruns, which in turn tends to drive greater insurance claims activity as project stakeholders seek to recover funds to pay for cost overrun from various insurance products utilized on the project and by project stakeholders.

- Project Delivery Models – Over the past few decades there has been a migration away from design-bid-build in favour of design-build. Under design-bid-build the owner would procure the design, and often have a substantial amount of the design complete when the contractor bid the work, thus creating greater certainty around project outcomes. With the design-build model the cost of design is borne by each individual bidder and given the most of these design-build procurement models utilize a competitive bidding process, each bidder is reluctant to invest too much money in the design knowing there is a chance they may lose and potentially be unable to recover the investment they made in design. As a result many design-build contract prices are fixed with insufficient design and as a result they tend to have a greater likelihood of cost overrun. As referenced above, when there are cost overruns on a construction project the stakeholders often look to insurance and performance security products to determine if any costs can be recovered from these policies thus driving up losses suffered by insurers.

- Complexity of Projects – Similar to the uniqueness of the project, if the project is complex, it will drive a greater likelihood of cost overrun, and thus a greater likelihood of insurance and performance security claims.

- Shortage of Skilled Labour – Less skilled labour (both management and trades) leads to greater likelihood of events that lead to insurance and performance security claims.

- Owner Capacity to Understand Construction Risk – A major issue in today’s construction marketplace is the ability of project stakeholders (owner, contractor and designer) to create a well-balanced risk allocation for their construction projects. As mentioned above, the construction economy has a shortage of skilled labour, and so too does the owner community when it comes to individuals that truly understand proper construction risk allocation. With improper risk allocation and the inability to work through risk issues, due to a lack of knowledge and skills, the likelihood of cost overruns, and therefore insurance claims, increases.

- Catastrophic Weather and Impact on Overall Insurance Sector – The United Nations Office for Disaster Risk Recovery has noted that 2000 to 2019 climate-related disasters increased by 83% compared to the previous two decades. Further Munich Re has indicated that in 2021 insured losses from natural disaster were about $120 billion which is well above the past 20 year average of $97 billion per year. Either way, the underlying insurance marketplace is being hit very hard by catastrophic events and these losses are a foundational root cause of the recent insurance market hardening.

- Linear Underground Risk – Several of the largest losses suffered by insurers on projects are related to civil project, specifically transit construction projects. These projects have substantial risk related to underground unknowns – soil conditions, utilities, unknown structures underground, and archaeological. These projects have been flag by insurers for property and professional liability losses given the frequency and severity of claims related to their execution.

- Inflation and Higher Interest Rates – As you can see from the previously referenced chart on the Survey of Business Obstacles, issued by the Canadian Construction Association, top obstacles are inflation and higher interest rates. More than half of those surveyed cite inflation as a major obstacle. Higher inflation and related higher interest rates drive greater uncertainty for construction projects and also drive down construction demand. Both of these issues are linked to insurable losses as various project and practice insurance and performance security policies show increased frequency and severity of claim when these two metrics are increasing.

OVERVIEW OF CURRENT CONSTRUCTION INSURANCE MARKET CONDITIONS

After a tumultuous five years of hard market conditions, there are positive indicators in 2025. A review of combined loss ratios shows many insurers are back in a profitable position due to underwriting discipline and better returns on their insurance investment vehicles. The hard work that began in 2019 has led to a stabilized market with ample capacity available for construction risks. Given the construction trends noted above, we expect that underwriters will continue to push underwriting discipline, so it is imperative that insureds are prepared to provide as much risk detail as possible, with a strong focus on risk mitigation and control. As is the case as the market transitions, some lines have become more competitive than others as evidenced below:

| Property/Builders Risk |

|

| Casualty/Wrap-up |

|

| Project Specific Professional Liability |

|

| Environmental Liability |

|

| Surety |

|

| Subcontractor Default Ins. |

|

While 2025 offers opportunities for insureds, challenges remain, including geopolitical risks, elections, climate-related losses, and economic uncertainty. To secure the best insurance outcomes, insureds should:

- Provide thorough and accurate underwriting data

- Invest in IoT for loss mitigation and data tracking.

- Implement strong water and fire mitigation plans.

- Prioritize contractual delivery models that foster collaboration.

PLATFORM is available to discuss these topics further.

Questions? Contact:

Jeff Saranko | Senior Vice President

Construction Industry Group

(437) 962-0985| jsaranko@platforminsurance.com

Clark S. Thomas | Managing Director

Construction Industry Group

416-524-0311 | cthomas@platforminsurance.com

Rick Schrank | Senior Vice President

Construction Industry Group

437-962-4087 | rschrank@platforminsurance.com